Last week’s article focussed on identifying and understanding the actual causes of economic loss in the context of intervening events. Over the course of the next two articles in our COVID-19 economic loss quantification series, I look at how intervening events influence approaches to solving the “but for” problems of economic loss.

In substance, the “but for” case presents the likely outcome of a future scenario had an event not occurred. In many instances, a single future “but for” scenario is sufficient. However, where a dynamic relationship exists between the “primary event” (being the event that occurs first) and the “intervening event” (being the event that occurs after the primary event), the number of potential “but for” scenarios expands, increasing complexity in assessing economic loss.

Fundamentally, the increase in complexity is due to two key interdependent variables: the knock-on effects of the intervening event on the plaintiff (for example, the impact of social distancing requirements on buying behaviours) and the ways in which the plaintiff may have responded to those knock-on effects (for example, shifting to online sales). While the plaintiff’s actual responses can largely be ascertained from historical data, the possible “but for” outcomes are better assessed through scenario analysis.

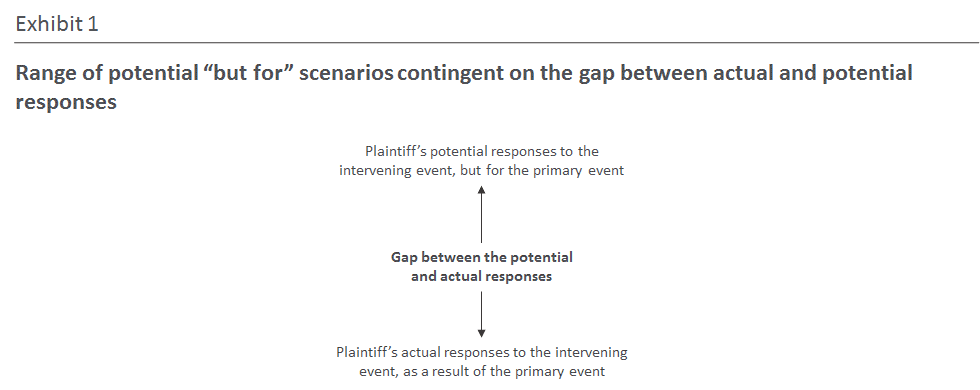

Exhibit 1 illustrates the “gap” that emerges between actual responses and the range of possible actions drives the extent and nature of the “but for” scenarios required. The plaintiff’s actual responses to the intervening event effectively create a “floor” or lower boundary for the scenario analysis. The upper boundary of the scenario analysis is determined by the range of the actions that were available to the plaintiff, but for the primary event.

To put this in context, let’s return to the example in last week’s article. If you recall, the defendant’s actions (the primary event) caused a 45% reduction in manufacturing capacity, which later slumped to 25% due to COVID-19 (the intervening event). In response to the

primary event, the plaintiff reduced the scale of the Manufacturing and Sales functions; following the intervening event, the plaintiff found a local supplier allowing it to recommence manufacturing. In that example, the plaintiff’s mitigating actions establish the floor to the scenario analysis (as no further operating model changes were implemented).

This leaves the following problem to be solved: in what ways might the plaintiff have responded to COVID-19, but for the primary event?

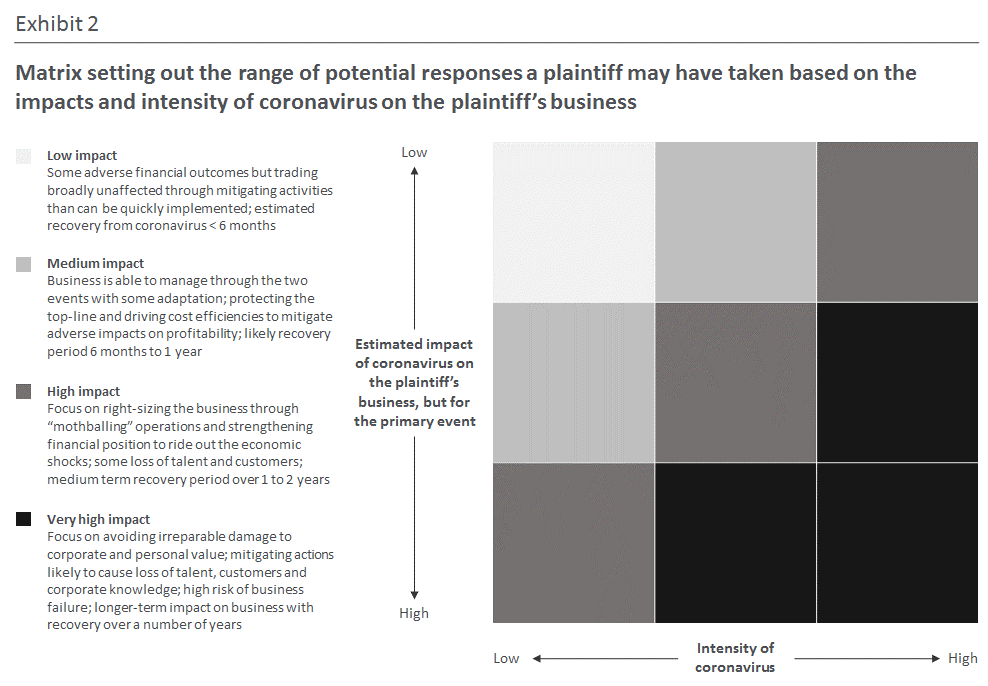

Exhibit 2 presents a scalable tool for solving the problem stated immediately above. In the current example, the “but for” scenarios are determined to be a function of the impacts and intensity of COVID-19 on the plaintiff’s business (where intensity refers to the duration and severity of coronavirus restrictions relevant to the plaintiff’s business). The overall (65%) slump in manufacturing capacity suggests that COVID-19 would likely have had a high impact on the plaintiff’s business. While the intensity of COVID-19 cannot yet be determined, the plaintiff’s likely responses fall within the high impact and very high impact categories using the matrix below.

From a financial modelling perspective, using tools like this focus me on surfacing and defining the key variables that drive material outcomes, in turn, keeping my financial models as simple and as commercial as possible. But I’m getting ahead of myself. I’ll discuss the modelling of scenarios in the next instalment of BRI Ferrier’s COVID-19 economic loss quantification series.

Need advice?

Early forensic accounting input may assist in developing the best legal strategy. We may be able to give a broad overview of the main issues after a brief review of available financials and an outline of the background to the matter. We aim to help, so please feel free to contact:

Paul Croft Jacqueline Woods

pcroft@brifnsw.com.au jwoods@brifnsw.com.au

+61 418 411299 +61 417 472668