When shareholders or partners go their separate ways, disputes often arise over the value of commonly held assets. In my valuation experience, some of that friction occurs because the parties involved don’t understand two commonly misunderstood concepts in business valuation, Enterprise value and Equity value.

To eliminate one of the sources of dispute before it erupts, this article explains the key difference between Enterprise value and Equity value, and the circumstances in which each value is relevant.

For simplicity, I have used the example of a business operated through a corporate entity, although the concepts apply equally to businesses operated through alternative trading vehicles such as trusts and partnerships.

Goodwill: the unreported asset on your balance sheet

As we all know, the balance sheet reports a company’s assets and liabilities acquired during the course of conducting its business. The assets and liabilities used to operate, and generated by, the business will be included in the balance sheet, except for one thing: should you be running a profitable business and generating a significant return to shareholders, the one asset that you won’t see on your company’s balance sheet is the market value of the business’ ability to generate that return – often referred to as “Goodwill and other intangibles” (but which, for simplicity, I’ll just refer to as “goodwill”).

Why not, I hear you ask? Put simply, accounting standards were introduced back in the mid-1990s to stop companies recognising “internally generated goodwill” at often inflated and unsustainable values, which put the kybosh on some pretty sketchy corporate and accounting practices that, among other things, rewarded corporate executives, contributed to the “tech bubble” and saw shareholders bear the brunt. But that’s a story for another day…

Enterprise value

Enterprise value is the term used to describe the value of the business as a whole. There are a number of methods commonly employed by valuers to determine the Enterprise value of a business (also a topic for another day). The key take-away is that Enterprise value comprises two components:

Net tangible business assets

It’s important to understand that “net tangible business assets” encompass only those tangible assets and liabilities that are intrinsically linked to generating the earnings of the business. For example, net tangible assets should include a normal level of working capital (such as raw materials, finished goods, trade and other debtors, trade creditors, accrued expenses and employee liabilities) and the net realisable or market value of plant and equipment utilised in the business.

Net tangible business assets do not include excess cash reserves, other assets owned by the company which are not an intrinsic part of trading operations, and any debt and other non-business-related liabilities.

Goodwill

Once the Enterprise value has been estimated, the value of the goodwill can be derived easily by deducting the value of the net tangible business assets from the Enterprise value. We now have the value of that additional asset that can be included on the balance sheet for the purpose of resolving the valuation dispute.

Generally speaking, if the business has consistently generated losses, is currently operating at a loss and is forecast to continue to do so, there is unlikely to be any goodwill in the business. However, there may be some value in other intangible assets such as customer lists, patents etc that might need to be separately considered.

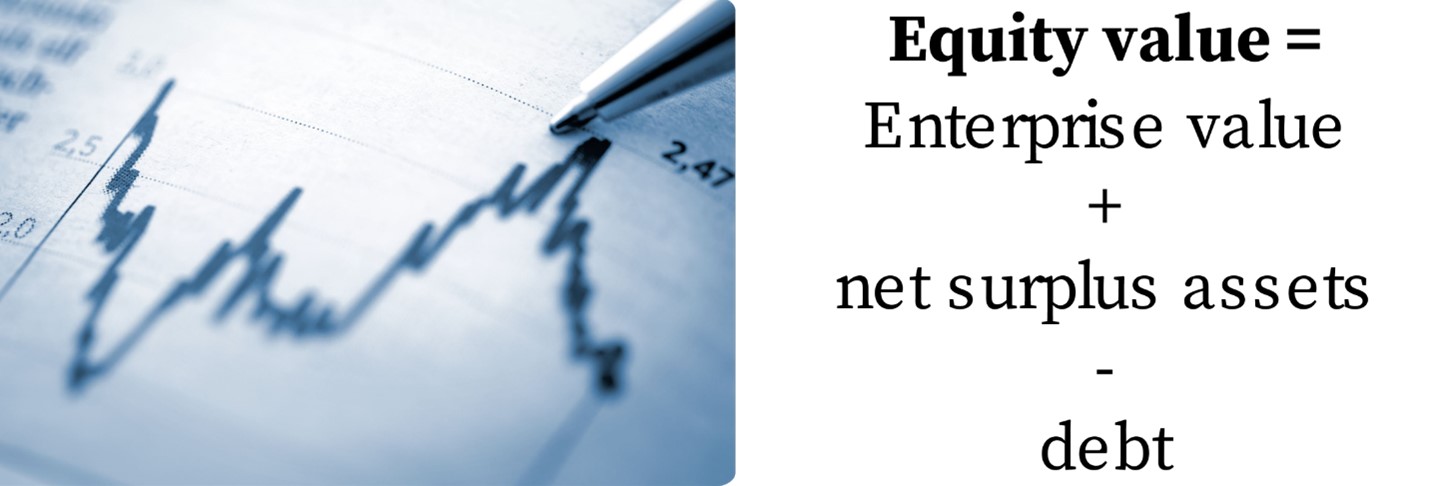

Equity value

Equity value is the term used to describe the value of the issued shares in the company, or in other words the underlying interest of the owners of the entity operating the business. Equity value is calculated as follows:

Essentially, net surplus assets comprise all other assets not included in net tangible business assets (defined above). Net surplus assets often comprise cash reserves over and above normal working capital needs, company investments and loans to related parties.

The distinction between business and surplus assets is not always crystal clear and evident from the balance sheet. For example, in most circumstances, the market value of the warehouse owned by the company is treated as a surplus asset, rather than as a business asset, because the decision to buy the warehouse represented an investment decision and it is possible to sell the business but keep the warehouse as a commercial rental property. In those situations, the machinations to arrive at Enterprise value need to include a notional rental cost.

Historically, the balance sheets of small companies might also include intangible assets such as formation costs. As those assets do not generate future economic benefit for the company (ie have no value), and technically therefore, fail to meet the accounting definition of an asset, such assets are usually excluded from the calculation of net surplus assets.

Debt comprises liabilities such as bank loans, historical tax liabilities (GST, income tax), equipment financing loans and loans from related parties.

Boiling it all down, you can think about Equity value as being equal to:

- All of the net assets represented on the balance sheet, adjusted to market value, plus

- The estimated value of goodwill.

What value should be used: Enterprise value or Equity value?

And this is often where the confusion sets in because it’s the wrong question being asked. The critical question is not what value should be used, but what is being bought or sold, notionally or otherwise?

Possibly for the only time in valuation, there is a straight-forward and indisputable answer:

- Use the Equity value if you’re buying some or all of the shares in the company, or obtaining a value of a party’s equity interest in his/her trading entity (in the case of family law disputes and shareholder oppression matters), or

- Use the Enterprise Value if you’re buying the business (that is, the trading entity retains ownership of surplus assets and debt obligations and there is no change in ownership of the company’s shares).

BRI Ferrier offers comprehensive expertise in business insolvency, personal insolvency, business recovery and turnaround, and forensic accounting. Our dedicated team understands the complexities of financial distress and provides practical, results-driven solutions tailored to each client’s needs.

With a presence in Adelaide and key locations across Australia, including Melbourne, Sydney, Cairns, Brisbane, Perth, Townsville, and Auckland, we are well-positioned to support businesses and individuals. No matter the challenge, BRI Ferrier delivers professional advice and strategic solutions to help regain financial control.